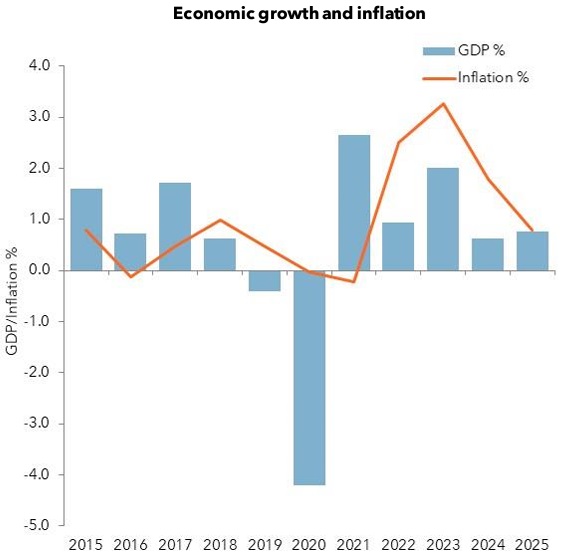

Economic growth and inflation outlook

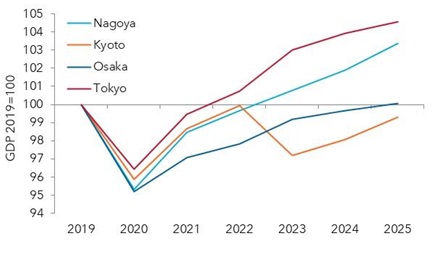

Aside from Tokyo and Nagoya, growth prospects are generally weak

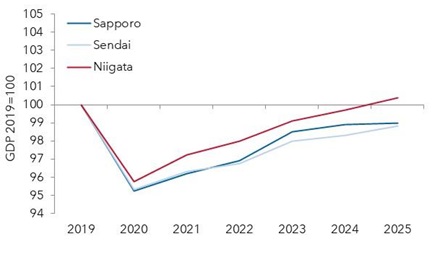

All three cities’ economies contracted by around 4% in 2020. Recovery has been slow in northern Japan. By 2025, GDP in Sapporo and Sendai is still expected to be around 1% less than it was in 2019. Niigata should perform a little better, with GDP finally moving above prepandemic levels in 2025. But its economy may be only 0.4% larger.

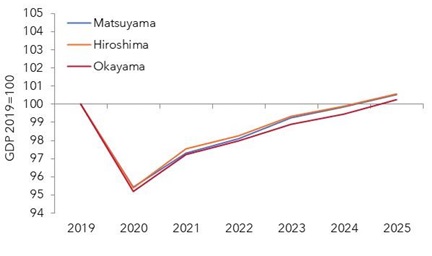

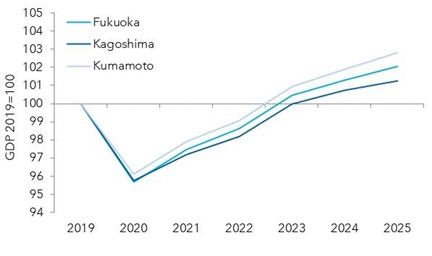

While all saw activity moved above 2019 levels in 2023, Kumamoto had the slightly stronger recovery. And it should lead the way through 2025, with GDP 3% larger than in 2019. Kagoshima will trail with an economy just 1% bigger by 2025.

Tokyo’s economy led the recovery, with activity restored by 2022. By 2025, its GDP should be 5% larger than in 2019. The prospects for Nagoya are also encouraging, with 3.4% expansion expected.

In contrast, Osaka’s economy may finally recover in 2025. Kyoto, having suffered a reversal in 2023, may still be more than 1% from recovery in 2025.

Japan’s air travel market

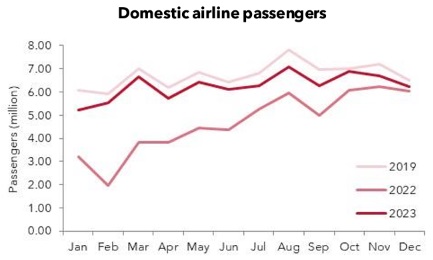

Domestic air travel demand recovery has stalled

Almost 81 million passengers flew on domestic air services within Japan in 2019. By 2021, demand had dropped by more than 60% to just over 30 million.

Real progress towards recovery was made during 2022. At the start of the year, passenger numbers were still 47% below their pre-pandemic level. By the end of the year, the deficit had been cut to just 7%.

Since then, the market has found it difficult to secure a full return of domestic passengers. Throughout 2023, their numbers have remained below 2019 levels, with little sign of the gap narrowing. Despite rising by 34% year-over-year, domestic travel in 2023 was still 7% away from a full recovery. Demand growth is also losing momentum, with the pace of expansion slowing to 7% in November and to just 3% in December.

One encouraging sign of normality returning to the market, however, is that seasonal patterns in demand appear to have been largely restored.

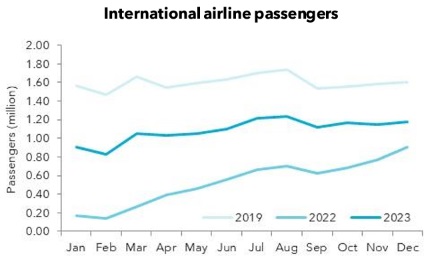

International demand still a long way from recovery

Because of the overhang of restrictions on travel, the recovery in international demand has been much slower.

During 2021, international passenger numbers fell to just 7% of their pre-pandemic level. By the start of 2022, they were still down by around 90%, although the year ahead was characterized by a steady recovery. This left demand 43% below 2019 by December.

Progress towards recovery was much slower during 2023, despite demand more than doubling year-over-year (YoY). By December 2023, international air travel was still more than a quarter lower than in the same month in 2019. And the pace of YoY growth slowed markedly during the year, slipping to 30% by December.

Preliminary numbers from ANA show YoY growth continuing at around 30% at the start of 2024.

Recovery in airline capacity

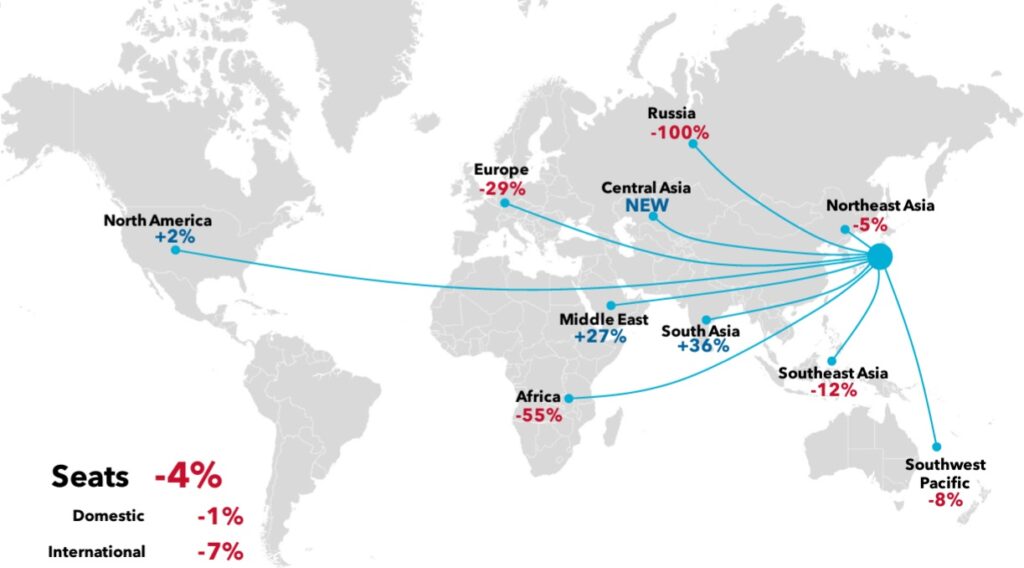

Airline capacity is below pre-pandemic levels in many markets

Domestic airline capacity in February 2024 was just 1% lower in Japan than in the same month in 2019. International capacity was further from recovery at 7% lower, although airline seats were already some way above pre-pandemic levels in three regions.

South Asia has seen the biggest postpandemic expansion in capacity, with airlines offering 36% more seats. While there have been modest increases to India and Sri Lanka, growth has been driven largely by new connections to Bangladesh and Nepal.

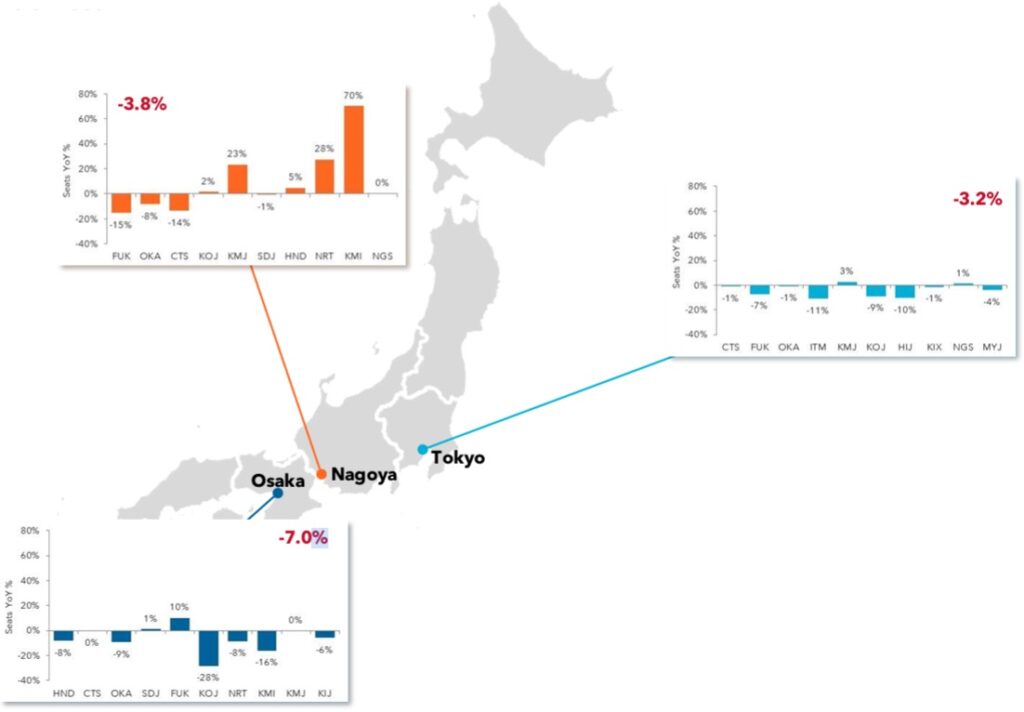

Growth in domestic air capacity

Across Japan’s three largest markets, domestic seats are 3-7% lower

Domestic seat capacity across three of Japan’s largest markets was down by 4% year-over-year (YoY) in February 2024. While seats from Tokyo (Haneda and Narita airports) and Nagoya (Chubu Centrair and Komaki) were 3-4% lower, Osaka (Itami and Kansai airports) recorded a deeper 7% decrease.

Among the airports most served from Tokyo, Osaka Itami (ITM), Kagoshima (KOJ) and Hiroshima (HIJ) have seen seat numbers decrease by around 10%. But capacity has increased slightly Kumamoto (KMJ) and Nagasaki (NGS), whilst remaining stable to Sapporo (CTS), Naha (OKA) and Osaka Kansai (KIX) airports.

Air travel outlook

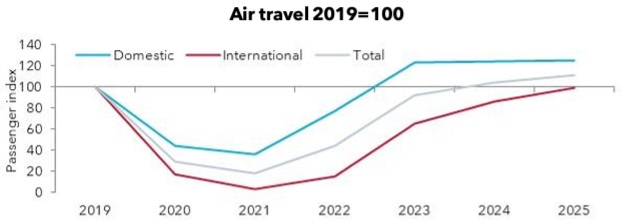

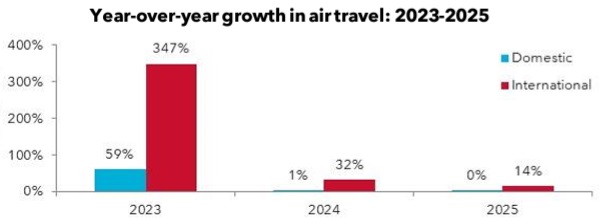

International recovery 2-3 years behind domestic

After falling to just 36% of their normal level in 2021, domestic passengers finally moved back above their pre-pandemic level in 2023, with strong growth pushing then 23% higher. But it seems the rebound in domestic demand will go no further.

While the return of international demand had started a year later, full recovery may occur two or even three years after the restoration of domestic travel. By 2025, Tourism Economics believes international demand could still be just short of a full recovery. While passenger numbers surged by 347% in 2023, the recovery seems likely to rapidly lose momentum. Domestic travel will fair even worse, recording virtually no growth in 2024 and 2025.

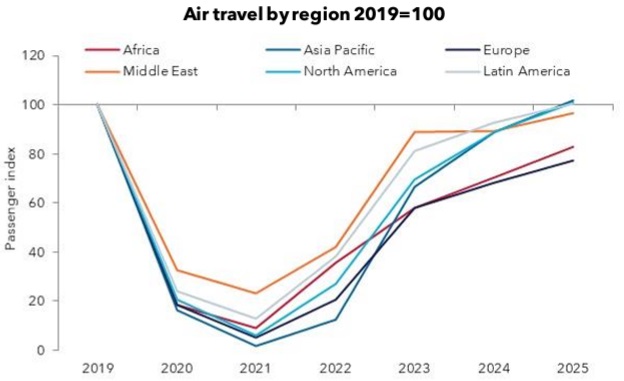

Asia Pacific leading recovery in international air travel

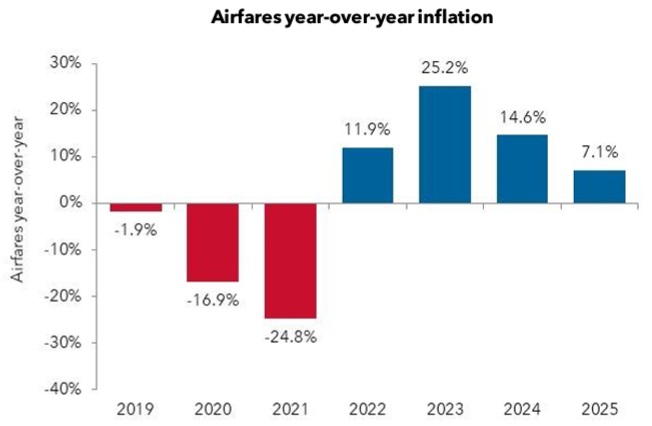

Airfares in 2023-2025

Hotel activity in the Japanese market

Average ticket prices in 2023

Short-haul fares lower year-over-year and vs 2019

The first half of 2023 had featured some strong year-over-year (YoY) movements in average ticket prices (ATPs) for short-haul travel, but this still left pricing below 2019 levels.

The situation changed dramatically in the second half, with fares lower in every month through November. This pushed ATPs one quarter lower than in 2019

Long-haul fares much higher than in 2019

In contrast to short-haul fares, pricing for long-haul flights was weaker YoY during the first eight months of 2023, with only modest rises thereafter. On average, fares were 3% lower during the 11-month period.

Due to some strong increases in 2020 and 2021, ATPs were above pre-pandemic levels throughout 2023, averaging 19% higher. However, this figure had eased to 11% by November.

Outlook through 2025

According to IATA data, Japanese airfares dipped by 2% in 2019. The market then endured two years of steeply falling ticket prices, with fares dropping by one quarter in 2021 alone.

Airfares rebounded with a 12% increase in 2022. Following Japan’s full reopening, travel’s recovery drove airfares 25% higher in 2023. While inflation should ease in 2024, IATA still forecasts a further 15% rise in airfares, easing to 7% in 2025. At this stage, airfares may still only be 7% higher than they were in 2019.

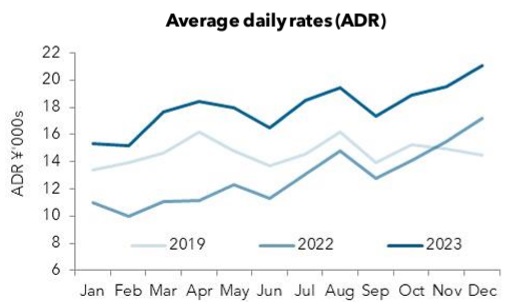

Strong rate recovery outpaces occupancy

Hotel occupancy made real progress in its recovery during 2022, starting the year at 44% and ending it above 75%. However, it remained below 2019 levels throughout 2023, averaging 74.2% for the year, compared to 82.3% in the pre-pandemic period. By December, occupancy was still around six-points from a full recovery, and it had dipped lower year-over-year.

The performance of average daily rates (ADRs) has been quite different. Even though occupancy had not recovered, by the end of 2022, ADRs had moved 19% higher than in December 2019. Room rates moved even higher during 2023, rising on average by 37% year-over-year (YoY) and to 23% above 2019. By the end of 2023, rate inflation had eased a little, but ADRs were still up 23% YoY.

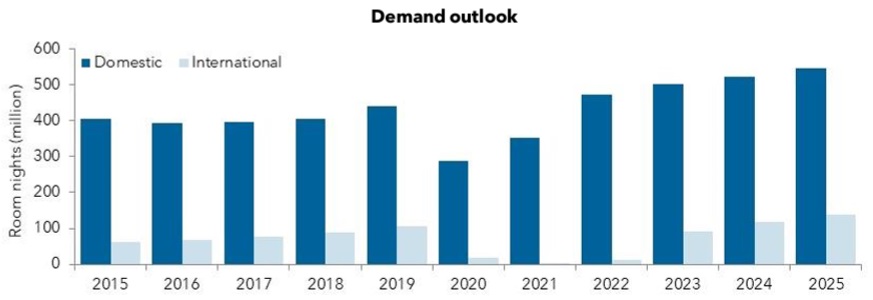

Total hotel room nights decreased by 44% in 2020. Domestic guests, who had previously accounted for more than 80% of demand, saw room nights move back 7% above pre-pandemic levels in 2022. A full recovery in international demand is expected in 2024 and should herald some strong growth. By 2025, room nights from international travelers should be one-third higher than in 2019, overtaking the one-quarter expansion by domestic travelers.

Total demand for hotel rooms in Japan is expected to rise by 8% in 2024 and 7% in 2025.

Hotel rates in key cities

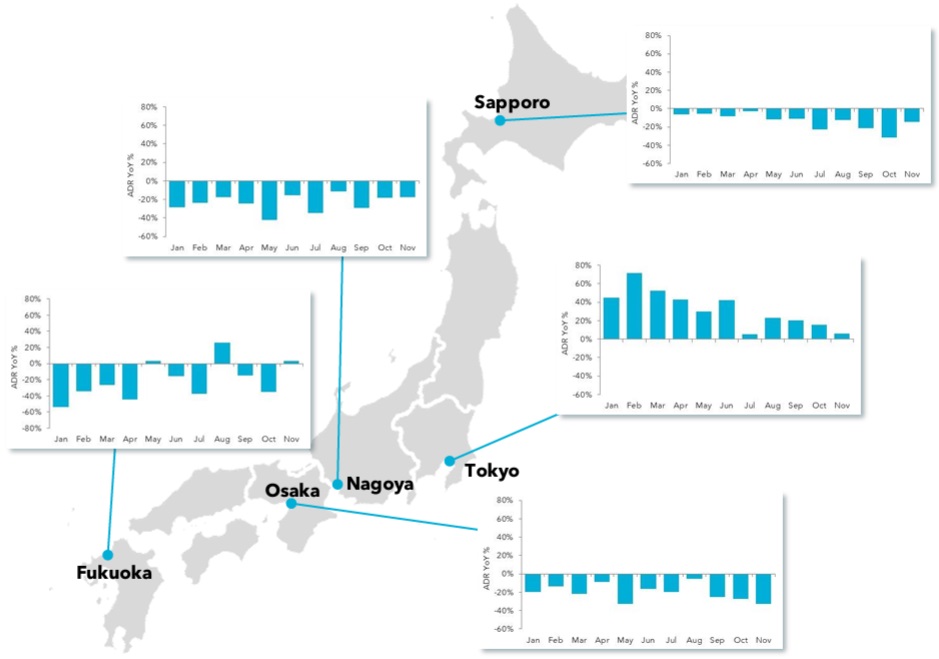

Tokyo bucked the trend of falling room rates during 2023

Corporate travelers saw average daily rates (ADR) for hotel accommodation in most of Japan’s largest cities decrease year-over-year (YoY) throughout 2023.

The clear exception is Tokyo, where ADRs have been increasing quite steeply ever since the middle of 2022. However, the pace of rate inflation moderated during 2023, easing from a peak of 70% in February down to just 6% in November. This slowdown is an inevitable result of the numbers cycling over some big increases in the previous year.

Among other cities, Sapporo’s hotels saw price decreases deepen as 2023 progressed, moving from January’s -6% to -14% by November. Osaka has seen a similar pattern: Decreases deepened from 20% at the start of the year to 33% by November 2023.

The situation is more varied elsewhere. Fukuoka saw a mix of price rises and falls during 2023, ending the period with November’s 3% rise. While prices fell throughout 2023 in Nagoya, the level of decrease ranged between 11% and 42%, depending on the month. After two months below 20%, there are tentative signs of rate deflation easing.