In this second edition of the Travel Market Report, we address the following issues:

- Six travel trends that will matter most in 2023

- Travel’s recovery and the headwinds it may face

- Airline consolidation and new entrants

- European airfares in key markets

- Hotel rates in Asia Pacific, Europe, Latin and North America

- The impact of major events on travel

- Travelers’ views on payment and expense

Travel Market Report

Welcome to the second edition of the Travel Market Report, brought to you by BCD Travel’s Research & Intelligence team.

In this quarter’s Travel Market Report, we address the following issues:

- Multiple organizations have presented their views on the trends they expect to play out in travel in 2023. We highlight six that we think will matter most.

- Travel is well on the way to recovery. But as we exit the pandemic, a wider range of issues may present headwinds for the recovery to navigate.

- As they exit one of the worst downturns in their history, airlines are beginning a new round of consolidation. But a queue of new entrants in the pipeline promises to bring new competition.

- In the previous edition of the Travel Market Report, we looked at U.S. airfares; now it’s the turn of European fares to go under the microscope.

- What’s happening to hotels? Have rates returned to pre-pandemic levels? How do they compare to last year’s level? The picture varies, so we take a closer look at what’s happening in Asia Pacific, Europe, North America and South America.

- Next year, Paris is due to host the Summer Olympic Games. What impact can a destination hosting such an event have on travel?

- What do travelers think of payment and expense? We explore the key findings of our recent global survey of business travelers.

The Research & Intelligence team

Mike Eggleton

Director, Research & Intelligence

Natalia Tretyakevich

Senior Manager, Research & Intelligence

Melina Sibaja

Travel Insights Analyst

Travel trends 2023

Six key trends for 2023

Multiple organizations have outlined the trends that expect to impact travel in 2023. Here are six trends that we feel will matter most in 2023.

Live for today The pandemic was a wakeup call to consumers, prompting them to reassess their priorities and attitudes to life. Today more people are living for the day, taking a short-term view when buying discretionary items, which include travel.

Spend smart Value-for-money has become more important to consumers amid financial instability and diminishing purchasing power. Cost-conscious buyers look for new shopping opportunities and re-distribute their spend.

Travel well Economic necessity has ushered in a new era of sustainable behavior. In response to growing concerns about climate change, the travel industry is taking action, changing the way it operates, albeit in small steps.

Sparking joy is a strong purchase motivator even when faced with rising prices. Hospitality and travel companies are primed to reintroduce fun and excitement away from home and help consumers attain a sense of normalcy.

According to Expedia’s Traveler Value Index 2023, 46% of people consider travel to be more important now than it was pre-pandemic. And 43% plan to increase their travel budget in the coming year.

Travel companies may support consumers’ last-minute discretionary spending by providing services on convenient terms, such as “buy now pay later”.

Travel prices are on the rise and are likely to impact consumers throughout the year and beyond. Few travelers are cancelling trips, but many are downgrading to cheaper alternatives. Thus, according to Skift Megatrends 2023 , 32% will spend less on food and activities while traveling.

Companies may be inclined to revise their travel policies as part of an increased focus on savings. To maintain their competitive positioning, the travel management companies that support them may need to introduce new pricing strategies and demonstrate their own value for money.

Today’s travelers put both the planet’s and their own wellbeing high on their list of priorities. They’re interested in purchasing sustainable health and mood-enhancing products. Travel companies are getting creative in response, increasingly accommodating both wellness and sustainability to align with travelers’ new values.

However, a significant gap exists between words and actions. According to Euromonitor Global Consumer Trends 2023, while investing in sustainability initiatives is a strategic priority for 45% of professionals, 41% cite consumers’ unwillingness to pay for them as their most significant challenge.

According to BCD’s Wellbeing survey, employer support for employees’ physical and mental wellbeing is very important to 85% of business travelers. Meanwhile, only 62% of travel buyers have wellbeing support measures for travelers in place.

Source: Euromonitor 10 Global Consumer Trends 2023; Skift Megatrends

Travel trends 2023

Born this way

Being on the cusp of financial independence, Gen Z consumers are about to transform the meaning of business as usual. Living in turbulent times, they take a cautious approach when selecting the businesses from which they purchase goods and services, and that includes travel.

A new risk reality

We live in a dynamic and often unpredictable world where change has become the new norm. Travel is no exception.

Humans or machines?

In the new age of Artificial Intelligence (AI), approaches to data, analytics and decision making are changing. Automation presents new challenges to human capital.

According to Euromonitor Global Consumer Trends 2023, 30% of Gen Z make purchase decisions based on brands’ social and political beliefs and 64% trust independent consumer reviews. A travel brand’s story increasingly contributes to sales. Trust is created when companies live up to their commitments (and damaged when they don’t).

Travel brands seeking to cater to the needs of the younger generation need to be aware of their values and needs, and offer services accordingly.

Post-pandemic, travelers have returned to an alarming reality of political, economic and social turmoil. New rules and safety measures are a source of everlasting concerns for travelers. For example, visa processing delays restrict international travel growth, particularly affecting emerging markets.

According to BCD’s Travel Risk Management survey , 41% of business travelers still worry about a pandemic or public health emergency while on a business trip.

Responding to travelers’ elevated concerns, travel brands may use insurance, trip protection and flexibility to provide peace of mind, build loyalty and drive revenue. Updated travel policies may increasingly allow the use of business class on planes and trains, airport lounges and pre-trip services, serving to alleviate traveler anxiety. Proactive communication can help travelers avoid unnecessary stress on the road.

Humans and machines need to be aligned to deliver meaningful solutions for consumers. Automation makes servicing faster and more convenient, but travelers may need a personal touch for specific tasks.

According to Euromonitor Global Consumer Trends 2023, 58% of consumers were comfortable talking to a human to address customer service questions. This was far higher than the 19% happy to talk to an automated bot on a company’s website in 2022.

Travel companies will be looking for the ways to use AI to assist human agents in servicing travelers on phone, in chat or via email. By handling simple tasks in real time, AI will save time, freeing up agents to focus on more complex tasks.

Labor issues and changing customer preferences offer opportunities for greater technology adoption. There is ample room for growth for travel companies that need to develop new strategies to address staff shortages.

Source: Euromonitor 10 Global Consumer Trends 2023; Skift Megatrends

Travel’s recovery and potential headwinds

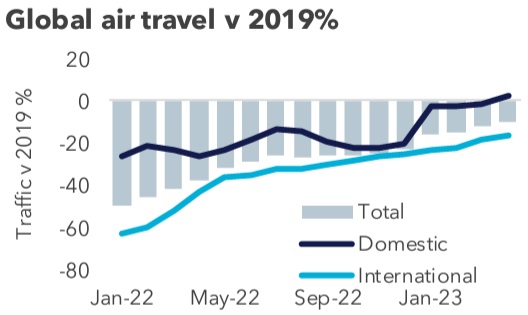

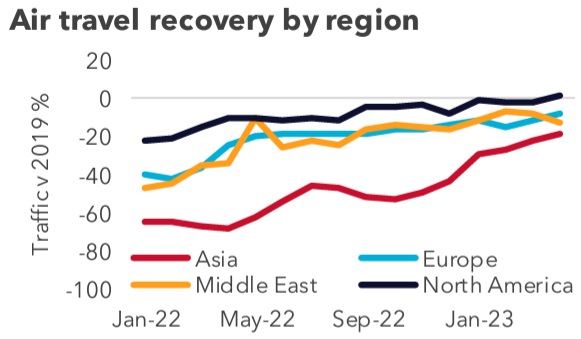

Asia’s reopening boosts the travel recovery

From mid-2022, the recovery in air travel lost momentum, with traffic stuck 25% below its 2019 level (chart left). This momentum was restored after China and Japan reopened at the end of the year. The size of the Chinese market gave domestic travel a clear boost. Globally, it moved 3% above its pre-pandemic level in April. International travel will take longer to recover, as airlines more slowly restore their services across Asia.

The reopenings helped propel Asia’s shortfall on 2019’s traffic levels from 44% in December to 18% by April (chart right). While recovery has resumed in Europe, with traffic 8% below 2019, the Middle East has seen its progress reversed. North America has finally delivered a full recovery, with traffic now 2.1% above its pre-pandemic level.

The recovery may need to overcome multiple headwinds

As we move forward towards a post-pandemic world, travel’s recovery faces a number of uncertainties. Business must once again navigate a world featuring multiple macroeconomic and geopolitical risks, instead of focusing on the single health risk that dominated lives for the last three years. Here are six headwinds to watch out for.

Ukraine conflict

The counter-offensive by Ukraine’s army has now started. The outcome is unpredictable, but it may well define the endgame in this conflict for both Russia and Ukraine and will have wider global ramifications.

Changing balance of power

With relations between the West and both China and Russia at new lows, a new Cold War era may have begun. The world will be a very different place to what we’ve become accustomed to over the last 30 years.

China decoupling

Western economies recognize the risks of an over-reliance on China. Decoupling or de-risking may provoke a reaction from China, which could interrupt investment, trade and ultimately travel.

Economic pressures

Consumers and businesses must contend with increased economic pressures in the shape of sharply higher inflation, rising interest rates and weaker growth. While the situation is starting to ease, the effects will take some time to unwind.

Wage price spiral

High rates of inflation are driving up wages, which could stoke it further, creating an upward spiral in prices. Interest rates may need to move higher and for longer to slow or reverse this cycle, adding to borrowing costs for both consumers and businesses.

A new banking crisis?

Prompt action prevented widespread contagion from Silicon Valley Bank’s collapse and a second round of bank failures in the U.S. Lending and investment may be curtailed until market confidence in banking is restored.

Source: charts: IATA Air Passenger Market Analysis

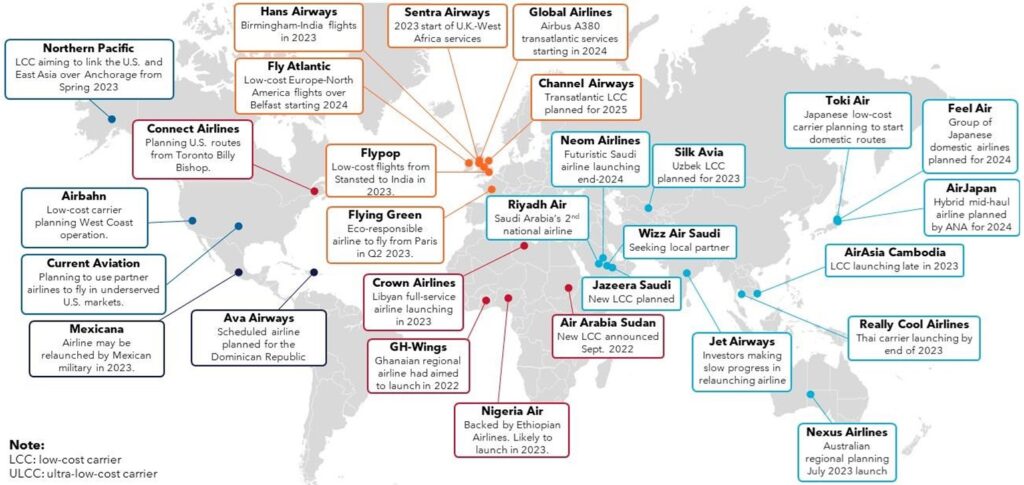

Airline consolidation or increased competition?

Consolidation gets under way

As we emerge from global aviation’s biggest downturn, a post-crisis consolidation is getting under way in the industry. In Asia, Korean Air and Asiana are awaiting approval for a merger that would create a carrier 204% bigger than its nearest local rival, while the combination of a refinanced Air India with AirAsia India and Vistara will much reduce competition in South Asia. In Europe, IAG is adding Air Europa as its third Spanish airline, joining Iberia and Vueling, and Lufthansa will secure a direct foothold in the Italian market after taking a 41% stake in ITA Airways. In the Americas, JetBlue’s merger with Spirit Airlines will firmly establish the new company as the 5th largest airline in the U.S., while Abra Group could challenge LATAM Group across Latin America by combining Avianca and Gol into a single airline group. But as mergers reduce independent airline numbers, new carriers continue to launch around the world.

Increased competition

Around the world, close to 30 airlines are presently in the pipeline at various stages in their start-up plans.

The U.K. has attracted a lot of interest from aviation investors, with six airlines in the pipeline. All seem to be banking on a boom in demand for long-haul leisure travel, with some also adopting the low-cost model. With Norse Atlantic already active in this space, it’s hard to see the market accommodating all six new entrants.

With travel a cornerstone of Vision 2030, Saudi Arabia’s economic diversification strategy, it’s not surprising to see four new Saudi airlines under development, split between low-cost and full-service operators. As well as providing a big boost to capacity in the local market, these airlines will likely challenge the Gulf carriers for traffic connecting over the Middle East.

While there’s a lot of activity, starting and sustaining an airline is never easy, as Flybe found out and the backers of Jet Airways are discovering. While some of these airlines will likely fail, others won’t, bringing new choice and competition to the market in a number of markets.

Source: BCD analysis

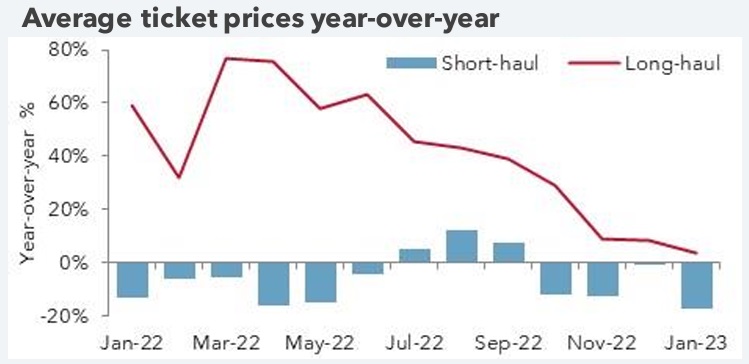

Airfares in key European markets

France

During 2022, average long-haul fares were 22% above 2019 and were still 15% higher in Jan. 2023. In contrast, short-haul fares averaged 10% below 2019 and started 2023 down even further at 19%.

Germany

Both long-and short-haul fares had tracked above 2019 for much of last year. While long-haul fares stayed 20% higher in January, short-haul fares suddenly dipped 8% lower, having lost momentum in previous months.

U.K.

In 2022, U.K. short-and long-haul fares averaged 13% and 18% above 2019, respectively. While long-haul fares remain elevated, staying 21% higher in January, short-haul fares slipped 9% below 2019 levels.

Year-over-year, a different picture emerges. Long-haul fares have fallen for three months and were down by 8% in January. Short-haul fares are now rising, increasing by 4% in both December 2022 and January 2023.

In 2022, long-haul fares rose on average by 24%, but by January 2023, prices were rising by just 2%. Short-haul fares remained essentially flat across 2022 and started 2023 in similar fashion, dipping by 2% in January.

Long-haul fares posted strong increases until mid-2022, before trending down to register a rise of just 3% in January. Outside of July-September, short-haul fares fell during 2022, and they remain weak, decreasing by 17% in January 2023.

Source: BCD Travel transactional data

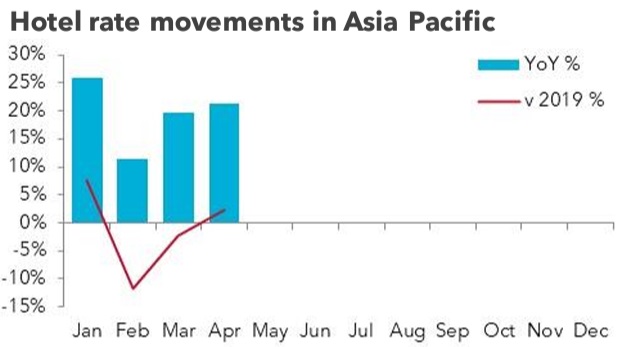

Hotel rates in Asia Pacific

Rate recovery taking hold

A rate recovery is now under way in Asia Pacific. During the first four months of 2023, data from STR shows hotel room rates rising 19% year-over-year across the region. They increased by close to one-fifth in both March and April.

Despite such strong increases, average daily rates (ADRs) so far this year have only matched the levels recorded during the same four months in 2019. After a weak performance in February and March, ADRs moved almost 4% above 2019 in April.

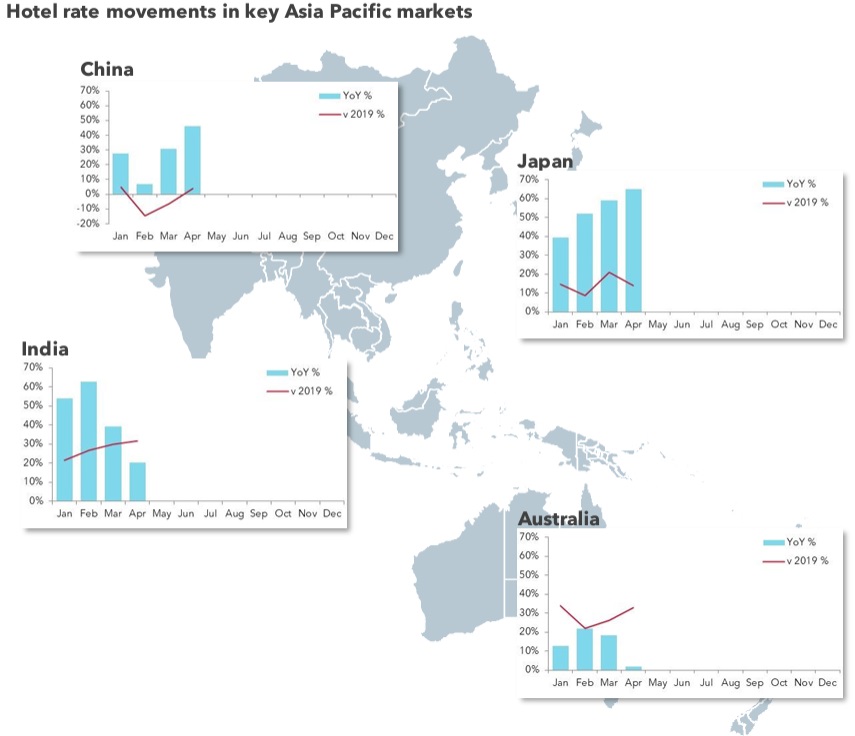

While these numbers point to a rate recovery, the situation is mixed across the region’s main markets.

Rates so far in Australia are running between one-fifth and one-third above their 2019 level. But April’s numbers suggest that year-over-year inflation may be losing momentum, with ADRs rising by just 2%.

China, which reopened at the start of 2023, has seen rate inflation quickly strengthen, reaching 46% in April, when ADRs also moved 4% above 2019.

Like Australia, India has also seen the pace of ADR increases weaken, dropping from 54% at the start of the year to 20% by April, although this still left ADRs +37% one-third higher than pre-pandemic.

In another recently-reopened market, Japan, year-over-year rate inflation has increased in every month, rising from 39% in January to 65% in April. ADRs are now 14% higher than in 2019.

Source: Analysis of data from STR

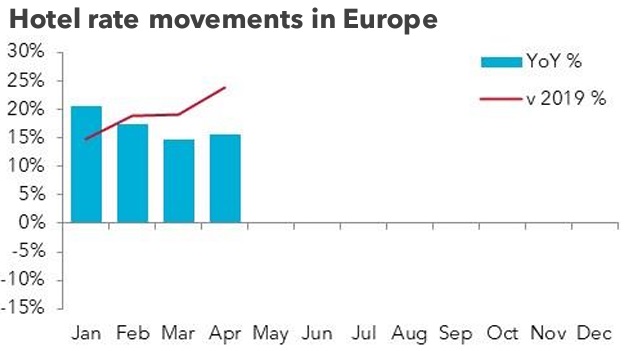

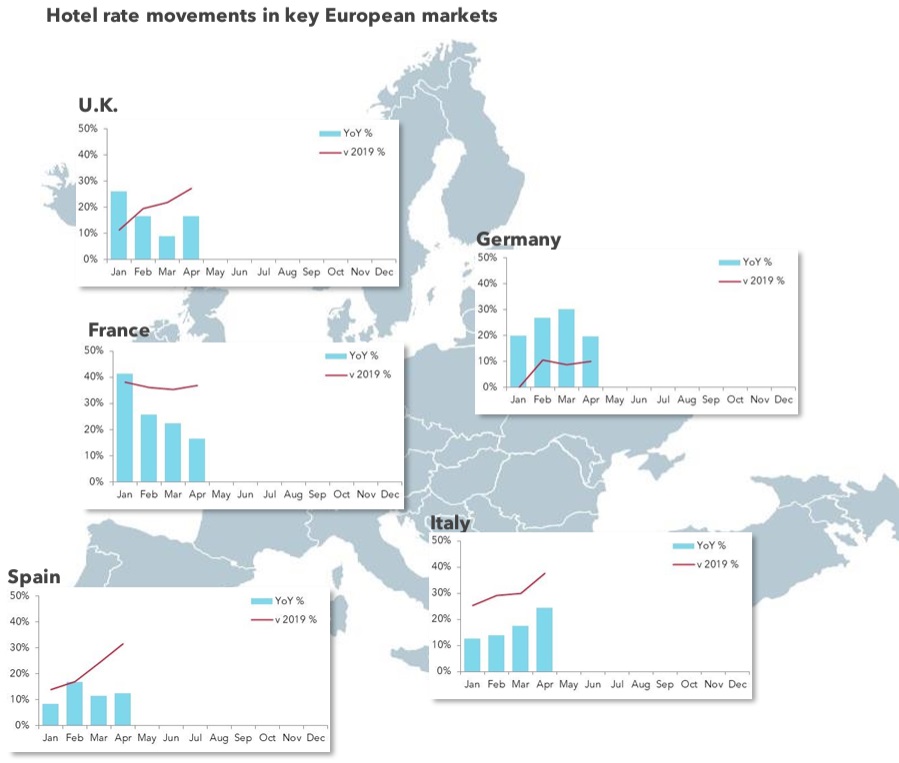

Hotel rates in Europe

Rates are moving higher v 2019

Since the start of the year, year-over-year movements in hotel average daily rates (ADRs) across Europe have eased from 21% in January to 16% by April, a level at which they appear to have stabilized in recent months.

Even though rate inflation has moderated, comparisons to 2019 levels have increased. By April, ADRs were almost one quarter higher than in 2019. So far in 2023, rates have been more than one-fifth higher.

Taking a closer look at individual markets reveals a lot of variation in ADR recovery across the region.

The U.K. comes closest to the regional average, with year-over-year ADR movements moderating but rising when compared to 2019. Rate inflation has also eased in France, falling from 41% in January to 17% by April, but inflation on 2019 levels has remained in a 35-38% range throughout 2023.

In Italy, ADR increases have strengthened this year, rising from 13% to 24% by April and this has also fed through to stronger increases on 2019 levels.

The rate environment has been steadiest in Spain, with increases close to 10% in most months, although pricing has become increasingly elevated relative to 2019 levels, surpassing 30% in April.

Germany has seen some of the strongest, sustained ADR inflation, averaging 23% so far this year, although rates are only 8% higher than in 2019.

Source: Analysis of data from STR

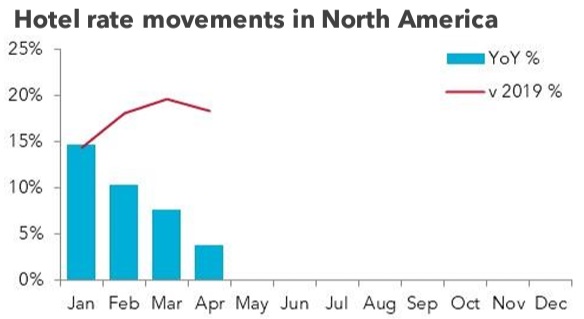

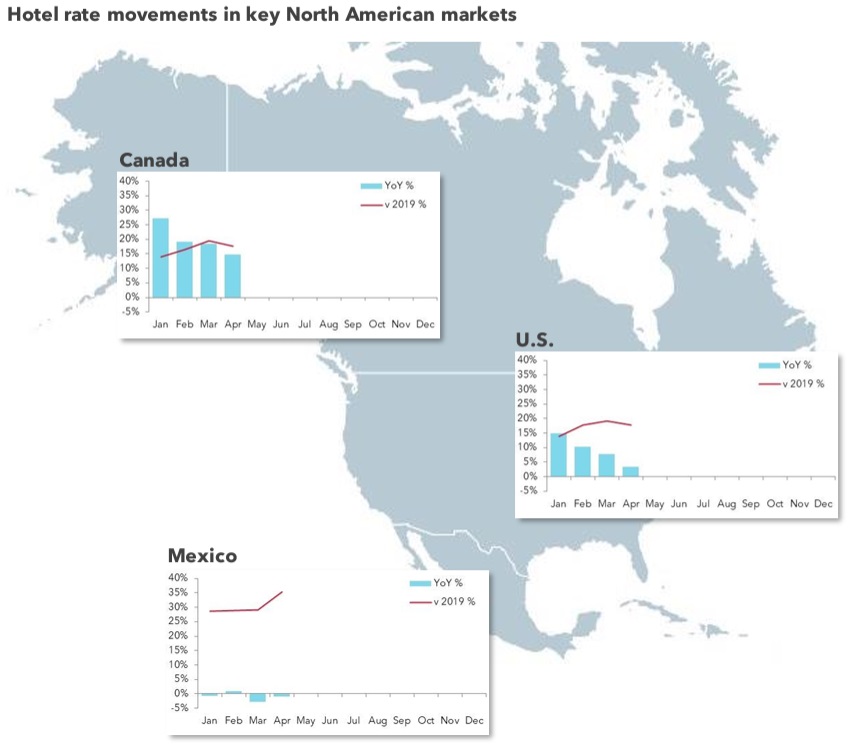

Hotel rates in North America

Year-over-year rate inflation is easing

In every month since the start of 2023, the rate at which average daily rates (ADRs) among North America’s hotels have been increasing year-over-year has decreased. From 15% in January, by April, rate inflation had eased to just 4%.

But when compared to pricing in 2019, ADR increases have remained high and show little sign of easing. So far in 2023, ADRs have been 18% higher than in the same period of 2019; a figure that hotels matched with their rate performance in April.

Among the three North American markets, only the U.S. has seen rate movements come close to mirroring the regional picture. Since January, year-over-year inflation in ADRs has fallen from 15% to just 3%. The sheer size of the U.S. market means it exerts a strong influence over the regional number. And like the regional situation, rates v 2019 in the U.S. remain elevated.

While ADRs in Mexico this year have been 30-35% above their pre-pandemic level, on a year-over-year basis, they’re risen by only 1% and decreased in both March and April.

Canada presents a different picture. While year-over-year price movements have eased this year, the rate of slowdown has been modest. This has ensured that ADRs have remained more than 15% above 2019 during the first four months.

Source: Analysis of data from STR

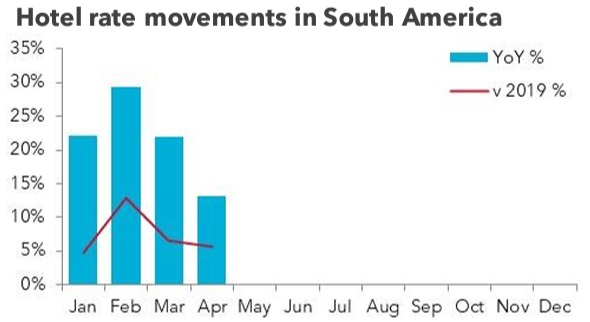

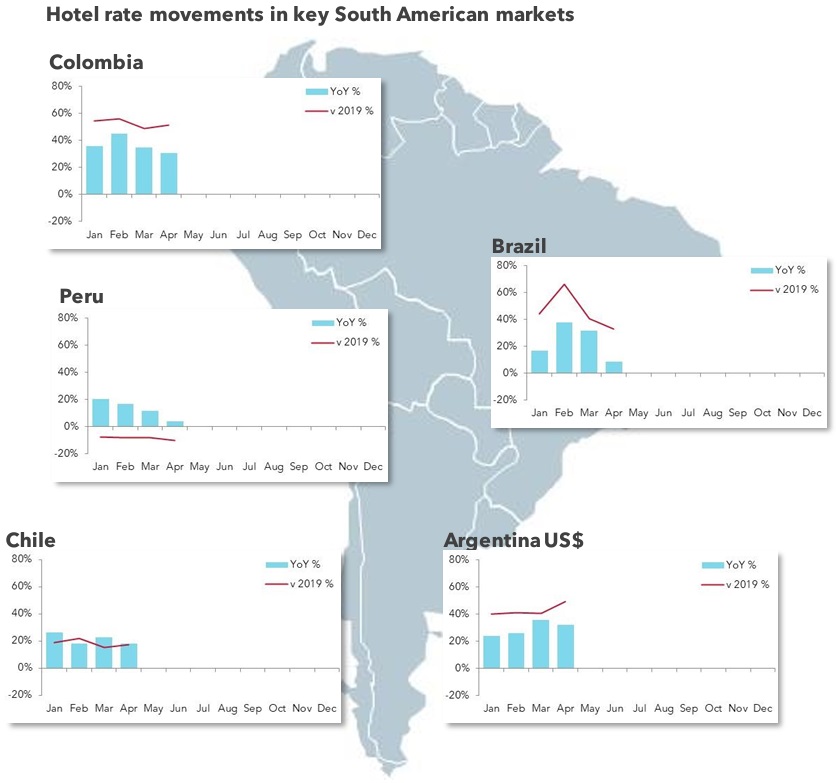

Hotel rates in South America

Rates are moving higher v 2019

After strengthening in February, year-over-year (YoY) movements in average daily rate (ADRs) across South America have eased in recent months. After hitting 29% in February, they’d fallen back to 13% by April.

When compared to their pre-pandemic 2019 levels, ADRs have followed a similar pattern featuring a spike in February. But the double-digit YoY increases that have characterized 2023 so far have still only resulted in ADRs that are 5% above their 2019 level.

Creating a regional view relies on aggregating ADRs denominated in US dollars. But if they’re left in local currency, a more varied ADR performance across South America is revealed.

At first glance, YoY rate movements seem to have stabilized at high levels in Argentina (dollar rates rising by more than 30%), Colombia (also at more than 30%) and in Chile (at around 20%). But increases have weakened in Brazil to 9% and in Peru to just 4%. In the latter market, April’s ADR was still below 2019’s level. With such low YoY price inflation, it’s hard to predict when hotel rates in +37% Peru will return to pre-pandemic levels.

In Chile, average daily rates have so far this year risen by around one-fifth both year-over-year and when compared to 2019.

Source: Analysis of data from STR

Impact of major events on travel

Travel is already impacted by regular events

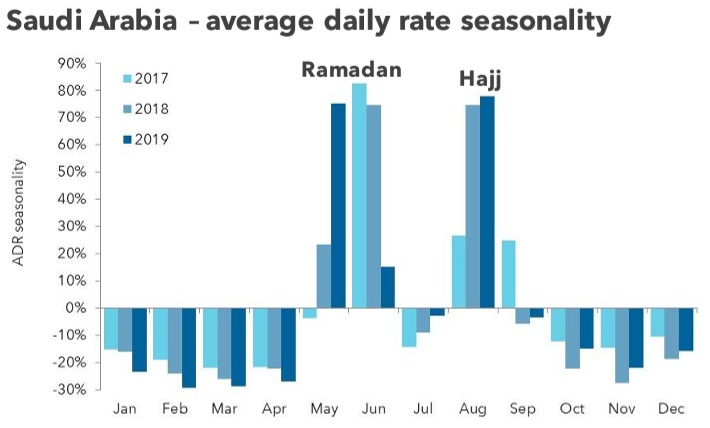

Regularly occurring events already have consequences for travel in many destinations, influencing the price and availability of the services travelers rely on, and most notably on flights and hotel accommodation. This is well illustrated in the Saudi Arabia market, where two annual religious events, Ramadan and the Hajj, cause dramatic rises in the average daily rates (ADRs) charged by the country’s hotels. During either event, travelers can expect to pay 60-80% more for a hotel room than in the rest of the year. And even between the two events, whose timing in the Gregorian calendar may vary each year, ADRs will be higher than in other months.

Similar seasonal effects are apparent in other countries, but these are more typically associated with summer sun or winter-sun leisure travel peaks, which put pressure on availability and pricing.

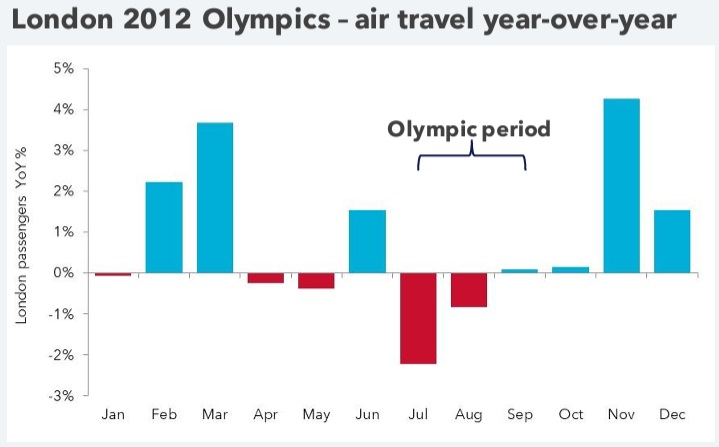

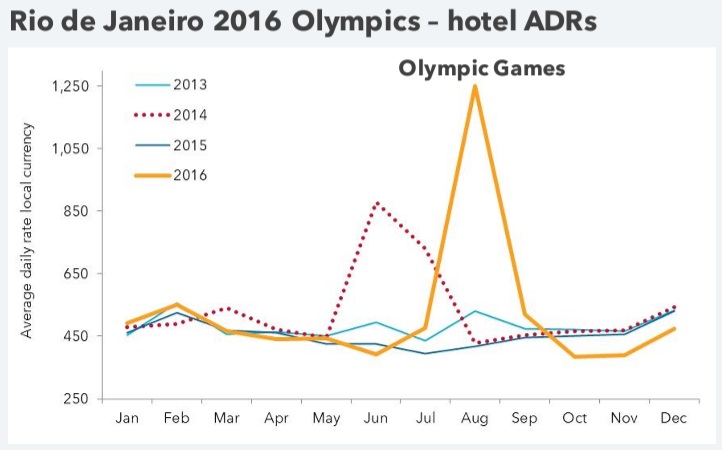

But what happens when a destination stages a one-in-a-lifetime event, as Paris will do next year, when it hosts the 2024 Summer Olympic and Paralympic Games? What can travel managers expect for availability and pricing? Taking a look at previous events provides some clues of what might happen to demand and prices.

How hosting a major event can impact travel

Hosting the Olympics did not have a material impact on London’s air travel market. In fact, with passenger numbers down 1-2%, some travelers may actually have stayed away during the Games.

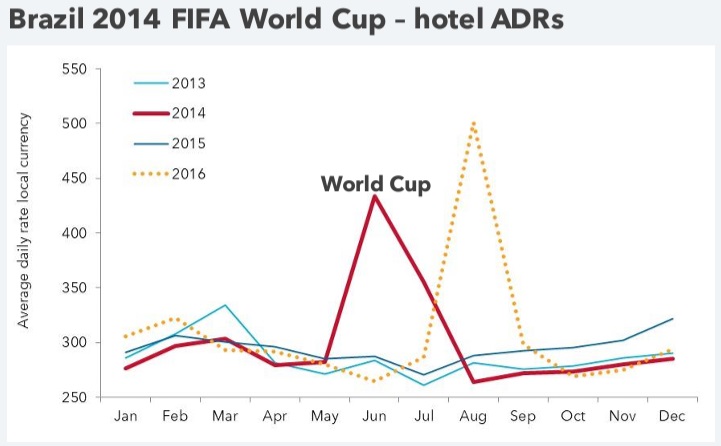

Hotel ADRs in Brazil were 45% higher than normal in June 2014, as the World Cup got under way. Upward pressure on room rates eased in July, as teams were knocked out and fans went home.

The Olympics’ impact was more dramatic, with August ADRs in Rio 239% above 2016’s average. But the length of the ADR spike was shorter, given that the World Cup was held over a longer period.

Payment and expense: the traveler view

Travelers share their views

How do travelers view payment and expense when traveling for business? What methods do they use to pay for their travel and the goods and services they use while on a trip? What pain points do they experience and what tools are there out there to address them?

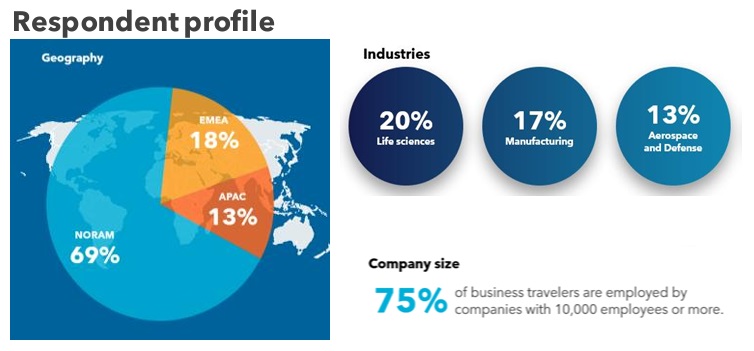

Intrigued to find out the answers to these questions, we surveyed a group of business travelers worldwide between March 31 and April 11, 2023. We received responses from 1,349.

While this was a global survey, more than two-thirds of respondents were based in North America, with almost one-fifth located in Europe. Three-quarters of all respondents worked for large companies with more than 10,000 employees. Travelers working in life sciences, manufacturing or aerospace & defense were well-represented.

Survey findings at a glance

Payment methods

Corporate cards are the most frequently used type of payment, as reported by 80% of travelers. Consumer cards are mentioned by more than a quarter of respondents. Just 1% of travelers use virtual cards, even though 26% are familiar with them.

Expense reporting

While 4 out of 10 travelers submit their expense reports right after returning home, a third may take days or weeks after the trip is over.

40% of travelers use a mobile app version of their expense tool.

Credit card fraud

Among business travelers, 1 in 6 have fallen victim to credit card fraud while on a business trip.

Most cases of fraud appear to have happened because of fraudulent charges being made by vendors or card-not-present fraud.

Payment pain points

Almost one-third of travelers find it challenging to stay within their company’s reimbursement policy. Other top pain points include paying for travel out of their own pockets, having cash in local currency and the risk of fraud. The good news is that one quarter of travelers claims to face no challenges around payment for travel.

Expense pain points

The time needed to be spent on expense reporting is travelers’ major expense pain point: A view expressed by 60% of travelers.

Half find it tricky to deal with receipts, citing the need to collect and expense them in different formats or keep the receipts after the trip is over as issues.

Find out more

These are some of the survey’s key findings, but you can find out much more in the full Surview report, Traveler Survey: Payment and Expense, which you can find here.

Source: BCD Travel survey, March 31-April 11, 2023